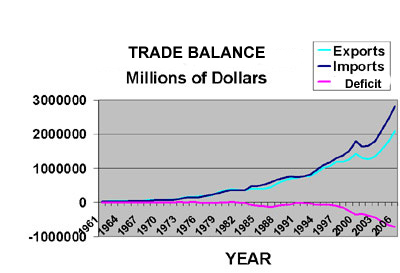

The credit crunch, failures of sub-prime loans, and bank bailouts are manifestations of the real problem. And what is the major problem? It is the trade deficit, which siphoned money out of the country and dictated an uncontrolled credit expansion to finance domestic spending. The trade deficit continues, but the credit expansion has reached its end. Two graphs tell the story. The first graph describes the trade balance of payments and shows the resulting deficit, which has grown steadily since the mid-1980s (except during the 1991 and 2002 recessions) and rapidly since the late 1990s. The present $900B trade deficit is still rising and cannot be easily contained. With manufacture of basic goods, such as clothing, electronics and plastics having been shifted to developing nations, the U.S. consumer presently has no alternative and must purchase these imported goods from external suppliers. Add a dependence upon imports for crude petroleum, steel mill products and refinery products and also the excessive consumption of imported raw materials and automobiles and we learn that the totality of reliance upon imports severely limits the domestic income and funds that are available for spending on domestic production.

The first graph describes the trade balance of payments and shows the resulting deficit, which has grown steadily since the mid-1980s (except during the 1991 and 2002 recessions) and rapidly since the late 1990s. The present $900B trade deficit is still rising and cannot be easily contained. With manufacture of basic goods, such as clothing, electronics and plastics having been shifted to developing nations, the U.S. consumer presently has no alternative and must purchase these imported goods from external suppliers. Add a dependence upon imports for crude petroleum, steel mill products and refinery products and also the excessive consumption of imported raw materials and automobiles and we learn that the totality of reliance upon imports severely limits the domestic income and funds that are available for spending on domestic production.

To compensate for the lack of domestic savings, the U.S. economy opened its gates to foreign savings. Foreign investment and purchase of U.S. Treasuries served to re-circulate dollars, which relieved the pressure on the dollar, and financed purchases of imports and domestic production. These mechanisms are only partial solutions to low domestic savings and cannot continue forever. The investments and their profits must be repaid and this is now happening. The Balance Of Payments Account can no longer be supported by foreign savings and investment, which means the U.S. has no supports for the flight of its jobs and capital.

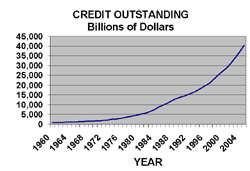

The shift of capital and manufacturing to the low wage nations has shifted purchasing power to the workers of these nations and decreased the purchasing potential of American workers. Maintainability of this shift is possible if the U.S. runs a positive balance of trade and foreigners purchase more U.S. goods and services. This has not been the case. Instead a continuous credit expansion has been used to finance an unsustainable trade deficit and the sales of domestic production. The next figure describes the credit expansion.

The Credit Outstanding curve shows steady growth since 1970 and accelerates rapidly after 1998, coincident with the time the trade deficit increased rapidly. Debt has obviously been used to finance imports and domestic consumption by substituting credit for the lack of internal purchasing power. The total debt, which consists of government, consumer, corporate and all other financial debt instruments reached $40T in 2004 and is now about $50T.

Federal government deficits, which have become unwieldy, financed a part of U.S. growth. Credit did the rest; fueling the seemingly perpetual motion economy of continuous growth. Theory predicted, as for all perpetual motion machines, it would soon grind to a halt. Adhering to the principle that “a rolling loan gathers no loss,” and utilizing artificially maintained low interest rates, creative financing, credit card expansion and finally sub-prime mortgages for the last batch of available spenders, system financiers increased the money supply and enabled purchasing power, especially for the home construction industry.

Free money, rather than free enterprise, more accurately characterized the U.S. economic system, which has been hit by a four times whammy:

(1) Credit markets have reached their limit,

(2) Foreign investment can no longer finance the trade deficit,

(3) The federal debt seems too high to support adequate fiscal stimulus plans, and

(4) A sizeable number of debtors cannot repay loans.

Read further The Trade Balance and the Limits of the Paulson Rescue Plan

Thursday, October 9, 2008

The Economic Catastrope

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment